For over two years, landlords throughout California have shouldered the financial burdens of eviction moratoria. Federal, state and local laws have limited the circumstances, manner, and time in which a landlord could remove a tenant delinquent on rent or other obligations under the lease. While some would argue these measures were a necessary health precaution during the worst of the pandemic, they shifted the financial burden of missed rental payments onto landlords in most respects. Now, landlords are finally experiencing some relief as eviction moratorium laws expire. Learn more about commercial landlord rights in California under current eviction regulations.

For over two years, landlords throughout California have shouldered the financial burdens of eviction moratoria. Federal, state and local laws have limited the circumstances, manner, and time in which a landlord could remove a tenant delinquent on rent or other obligations under the lease. While some would argue these measures were a necessary health precaution during the worst of the pandemic, they shifted the financial burden of missed rental payments onto landlords in most respects. Now, landlords are finally experiencing some relief as eviction moratorium laws expire. Learn more about commercial landlord rights in California under current eviction regulations.

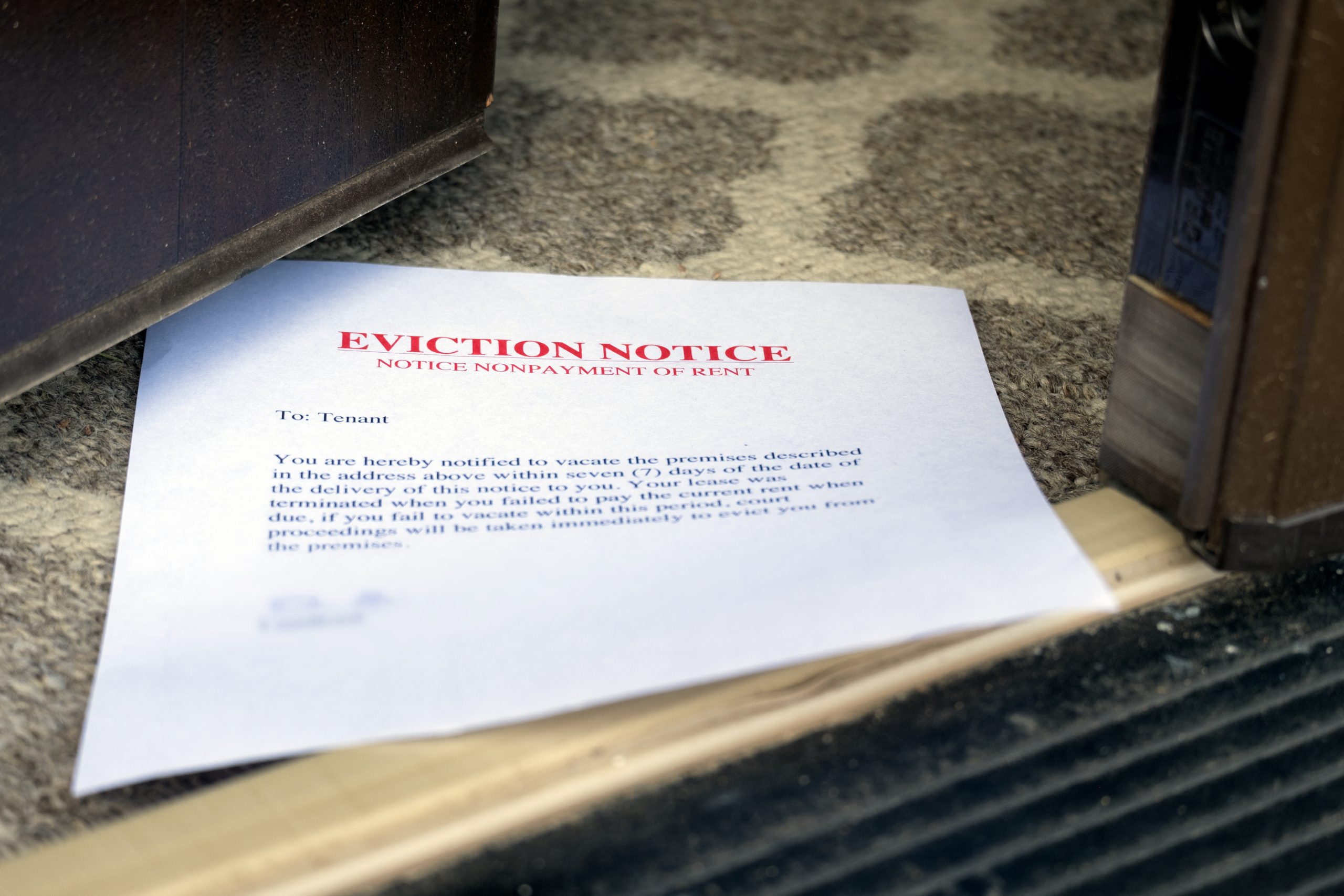

How California Has Handled Commercial Tenant Evictions

Governor Newsom’s latest executive order extended eviction moratoriums on commercial landlords through September 30, 2021. Since that date has lapsed, commercial tenants are no longer protected under the expired law and must rely on state and local regulations still in effect. In sum, commercial landlords may start eviction proceedings against tenants in the counties where no extension has been provided. In some counties, local ordinances have extended eviction moratoriums and protections. Los Angeles County, for example, has created a two-phase tenant protection resolution. Different eviction rules will apply as the procedures are phased in throughout 2022. In Santa Clara County, commercial tenants must now be caught up on at least fifty percent of their arrears, or they could be subject to eviction. Tenants have until August 19, 2022, to be fully paid up on their arrears. Each county has its own rules, so be sure to consult with an attorney about your specific situation.